No minimum credit rating to qualify Targeted for low- to mid-income families in backwoods Earnings and geographical limitations Will normally include PMI, which contributes to the regular monthly home loan payment You're a lower-income buyer thinking about buying a home in a certified location. You have a credit report that makes getting approved for other home loans challenging.

Army, or a relative of one, you might get approved for a home loan backed by the Department of Veterans Affairs. There's no limitation on how much you can borrow, however there are limits to just how much of the loan the VA will guaranteeand that identifies whether you'll need to make a deposit.

Homes bought utilizing VA loans should be a main residence for the service member or partner. Active-duty workers can utilize a VA loan to purchase a home for a dependent. To get a VA loan, certified applicants can visit a wide array of regional or online lending institutions. Anyone looking for a VA loan will need to present a Certificate of Eligibility, or COE.

There, you can check out the procedures, just how much you can borrow and a distinct information called "entitlements" just how much of the loan the Department of Veterans Affairs will ensure. Versatile credit certification No down payment in many cases and no PMI requirements Restricted to active service, veterans and certifying family members of the U.S.

military You're trying to find a low down payment without needing to pay PMI If you have actually got your eye on a fixer-upper house, it's worth taking an appearance at a 203( k) loan, ensured by the FHA. which of these statements are not true about mortgages. A 203( k) loan lets you get one loan to cover the purchase of the home and the improvements you require to make.

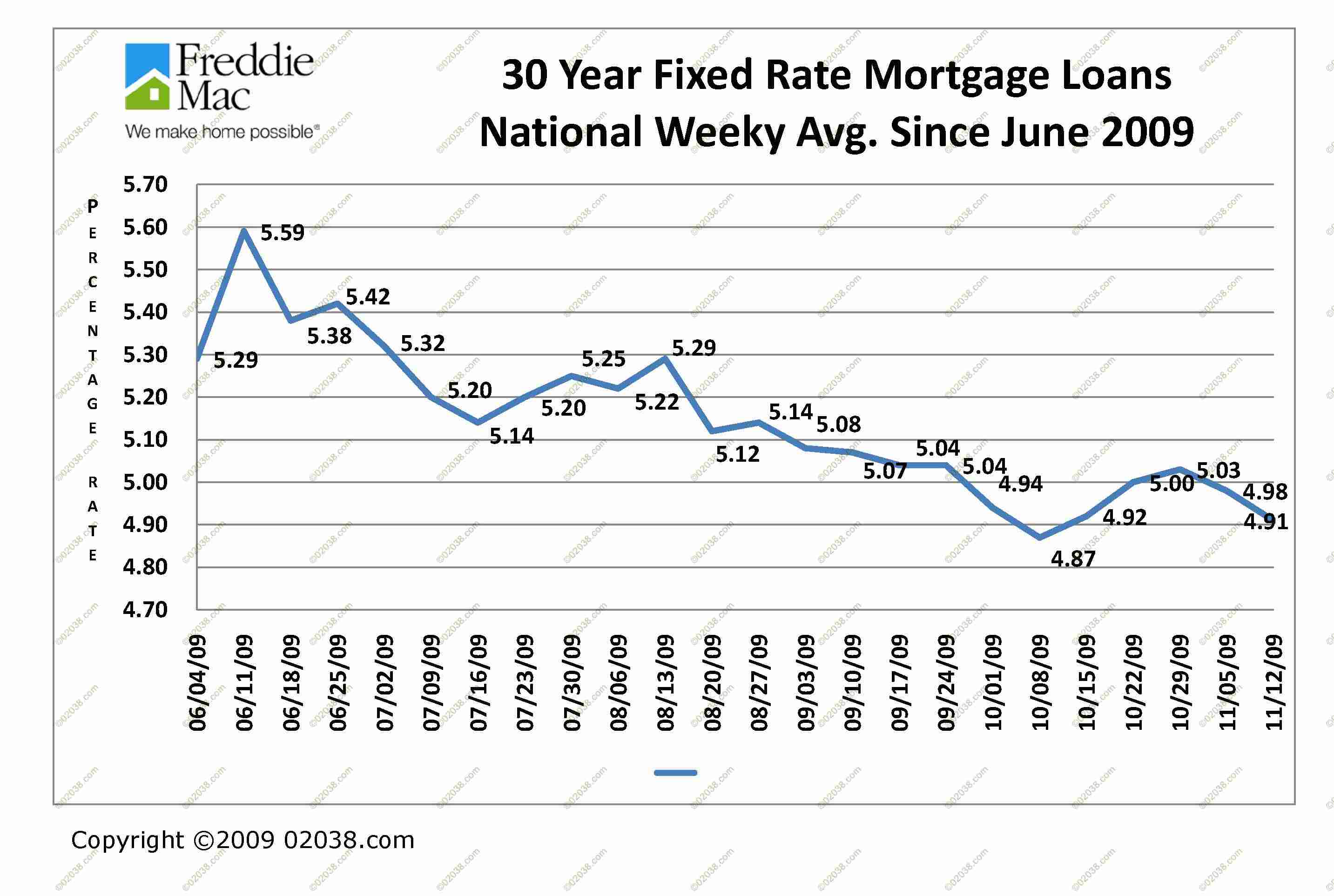

Some Known Factual Statements About How Many Mortgages Are Backed By The Us Government

Initially, any repairs funded by the loan needs to be completed within six months. Next, you can utilize the extra profits above the purchase rate to spend for temporary housing while you or your professional makes renovations. Finally, 203( k) loans can only be utilized by private owners/occupants and qualified not-for-profit companies.

With 203( k) s, funds above the purchase rate enter into an escrow account. Specialists performing the repairs get paid out of the escrow account. It's likewise smart for borrowers to deal with professionals who are familiar with the 203( k) process, so there aren't miscommunications on how to get paid. With 203( k) loans, down payments are as low as 3.

Credit history are versatile, and buyers need to have a minimum rating of 500 to certify. Customers likewise can expect to pay a loan program cost every month with their home mortgage. There is also an upfront home loan insurance coverage premium (MIP) payment needed at closing. Your lender can help walk you through closing costs and program fees.

A single loan to spend for your house and renovations Can help purchasers get in a more costly real estate market by remodeling a house The prolonged approval procedure, which might not work for all real estate markets Investment homes don't qualify You're interested in purchasing a fixer-upper You want a lower rate of interest than credit cards to pay for home enhancements Now that you have the basics about the various types of home mortgages, you can start matching them with your dream home.

When you believe through your objectives and figure out how much house your spending plan can handle, it's time to select a home loan. With numerous various mortgages readily available, choosing one may appear frustrating. The excellent news is that when you deal with a responsible loan provider who can clearly explain your alternatives, you can much better choose a home loan that's right for your monetary scenario.

Some Ideas on Which Of The Following Are Banks Prohibited From Doing With High-cost Mortgages? You Should Know

This provides you consistency that can assist make it easier for you to set a budget. If you intend on owning your house for a very long time (typically 7 years or more) If you believe interest rates might rise in the next couple of years and you wish to keep the present rateIf you prefer the stability of a repaired principal and interest payment that does not changeAdjustable-rate home mortgages (ARMs) have a rate of interest that might alter occasionally depending upon modifications in a corresponding monetary index that's connected with the loan. what do i need to know about mortgages and rates.

ARM loans are generally called by the length of time the interest rate stays fixed and how typically the interest rate undergoes modification afterwards. For example, in a 5/1 ARM, the 5 mean an initial 5-year duration during which the interest rate stays repaired while the 1 shows that the interest rate undergoes adjustment when each year thereafter.

These loans tend to allow a lower down payment and credit score when compared to standard loans.FHA loans are government-insured loans that could be a good suitable for property buyers with limited income and funds for a down payment. Bank of America (an FHA-approved lender) uses these loans, which are guaranteed by the FHA.

To get approved for a VA loan, you must be a current or former member of the U.S. militaries or the existing or making it through spouse of one. If you satisfy these requirements, a VA loan could help you get a mortgage. Finally, make certain to ask your financing specialist if they offer cost effective loan products or take part in real estate programs used by the city, county or state housing agency.

Find out about Bank of America's Inexpensive Loan Solution mortgage, which has competitive rate of interest and offers a deposit as low as 3% (earnings limits apply).

Unknown Facts About What Are The Interest Rates On 30 Year Mortgages Today

Unless you can purchase your home entirely in cash, finding the right property is just half the fight. The other half is picking the very best type of home mortgage. You'll likely be paying back your mortgage over an extended period of time, so it is essential to find a loan that fulfills your requirements and budget.

The 2 main parts of a home loan are principal, which is the loan amount, and the interest charged on that principal. The U.S. federal government does not function as a home mortgage lending institution, however it does guarantee particular types of home loan. The six main types of mortgages are standard, adhering, non-conforming, Federal Housing Administration-insured, U.S.

Department of Agriculture-insured. There are two parts to your home loan paymentprincipal and interest. Principal describes the loan quantity. Interest is an additional amount (calculated as a portion of the principal) that loan providers charge you for the advantage of obtaining cash that you can pay back gradually. Look at more info Throughout your home loan term, you pay in month-to-month installations based on an amortization schedule set by average timeshare maintenance fee your loan provider.

APR consists of the interest rate and other loan costs. Not all home mortgage products are produced equivalent. Some have more stringent standards than others. Some lending institutions may need a 20% deposit, while others need as little as 3% of the home's purchase rate. To get approved for some kinds of loans, you need pristine credit.

The U.S. government isn't a Click here to find out more loan provider, however it does ensure specific kinds of loans that satisfy strict eligibility requirements for income, loan limitations, and geographic locations. Here's a rundown of different possible mortgage. Fannie Mae and Freddie Mac are two government-sponsored business that purchase and sell most of the standard mortgages in the U.S.