For the letter itself, some lending institutions have standard kinds, however others do not. You can type up the letter yourself or ask your real estate representative or broker to help, but in general, you'll require to include: Your name and the name and address of the person making the giftThe amount that's being gifted to youThe address of the home you're buyingThe relationship of the person who's making the giftWhere the cash's originating from (i.

a bank account, cost savings account, financial investment account) A clear explanation that the cash is a gift, not a loan (obtained funds are not permitted deposit presents) Gifts are just permitted if they're from member of the family, not friends. An exception applies if you're engaged and your partner is offering the present.

For instance, the lending institution might ask to see a bank statement or other kind of evidence verifying that the donor has the money to present to you. A copy of a canceled check constructed out to you or paperwork showing an electronic transfer in between the donor's account and yours will work fine.

Whether you're receiving a check or an electronic transfer from your benefactor, make sure to deposit this money into a separate checking account apart from your monitoring or cost savings. You don't want to commingle gift funds with any of your other finances. Doing so might make complex the paper trail and trigger the loan provider to decline the present entirely.

Nevertheless, the individual making the gift to you can trigger a gift tax if the amount exceeds the annual exclusion limitation. For 2020, for example, moms and dads who are wed and submit a joint return can gift up to $30,000 per kid for a home mortgage deposit (or any other function), without sustaining the gift tax.

It's not constantly simple to blend household and financial resources. Make sure that accepting a gift is the best move for keeping your family delighted. The very best thing you can do is talk through the possible benefits, challenges, and the tax implications with the person or persons who are preparing to present the cash.

For instance, you might extend your timeline for buying and deal with saving cash. Or you may decide to offer things you own or begin a side hustle or company to develop additional cash circulation you can conserve. Deposit help programs are another alternative. These programs can offer grants and money help to help cover deposits and in many cases, closing expenses, for eligible property buyers.

Little Known Facts About What Are The Different Types Of Mortgages.

The regulations gift letters and funds can be rather confusing. To provide you a deeper understanding of the guidelines and reasons behind them, let's have a look at some frequently asked questions. The factor loan providers care if you've received a present is that it impacts their evaluation of how risky it is to lend you funds.

A big money gift can be deemed a warning, particularly if there's issue that the present funds do not satisfy regulations. The main issue for loan providers is that the present may actually be a casual loan that the donor anticipates to be paid back. If the gift is really a loan in disguise, you might have more debts than you can realistically pay off.

Even if you do not instantly report them, lenders can normally inform if you have actually received present funds. The reason loan providers have the ability to discover presents received is that your finances go through extensive evaluation timeshare exit in the underwriting phase of your home mortgage application. Throughout the application procedure, a home loan underwriter analyzes your finances, which includes timeshares for sale in florida cancellation examining your bank declarations.

Given https://sethdnrd120.shutterfly.com/48 that big presents are atypical, they're right away reported. Now, keep in mind that your lender will not expect you to have a gift letter for small quantities of cash you have actually gotten. For instance, you won't require to stress about a $50 check you got for your birthday - what is a hud statement with mortgages. However, loan providers will be looking for a description for any gift that is higher than half the worth of your total month-to-month household earnings.

For that reason, you would require a present letter to report any present of $2,500 or more. You don't need to fret about being penalized for receiving present funds. As long as the present follows the guidelines noted above, and you provide a gift letter to reveal it, receiving funds to help you pay for your deposit will not harm your chances of getting a mortgage.

Some types of loans allow 100% of the deposit to be a gift from a good friend or household member. If you do have somebody going to pay the deposit on a mortgage for you, you'll need a gift letter to accompany the funds. This post details which kinds of loans permit talented deposits, talented down payment standards, and a design template deposit present letter.

A recent research study performed by the Association of Realtors revealed that the third most significant difficulty prospective property owners are scared of is the down payment. how to qualify for two mortgages. Luckily, there are loans readily available that offer 100% financing without any down payment. Donations of down payments can be applied to mortgages on your main and second houses.

What Are Interest Rates Today On Mortgages for Beginners

Any Federal government or Private loan enables the down payment to be a gift from a friend or relative. Generally, lending institutions require that the donor have a household or marital relationship with the borrower. Depending upon the loan, the following generally function as acceptable sources of presents for borrowers: SpouseFiance or domestic partnersChild or dependentParentUncle, auntie, or other individual related by blood or marriageLegal guardianFor loans backed by FHA, a "close friend" who documents his/her "plainly specified" interest in the transaction will be enough.

Your lender will likely require a "gift letter for a home loan" signed by the donor. This constitutes one method your bank or mortgage company confirms that you're getting a gift, not incurring financial obligation. The present letter ought to contain: The name, address, and phone number of the donorThe donor's relationship to youThe dollar amount of the giftThe date of transfer of the funds for the giftState that the donor does not anticipate payment from youStreet address of the home being purchasedDownload this gift letter for a home mortgage here.

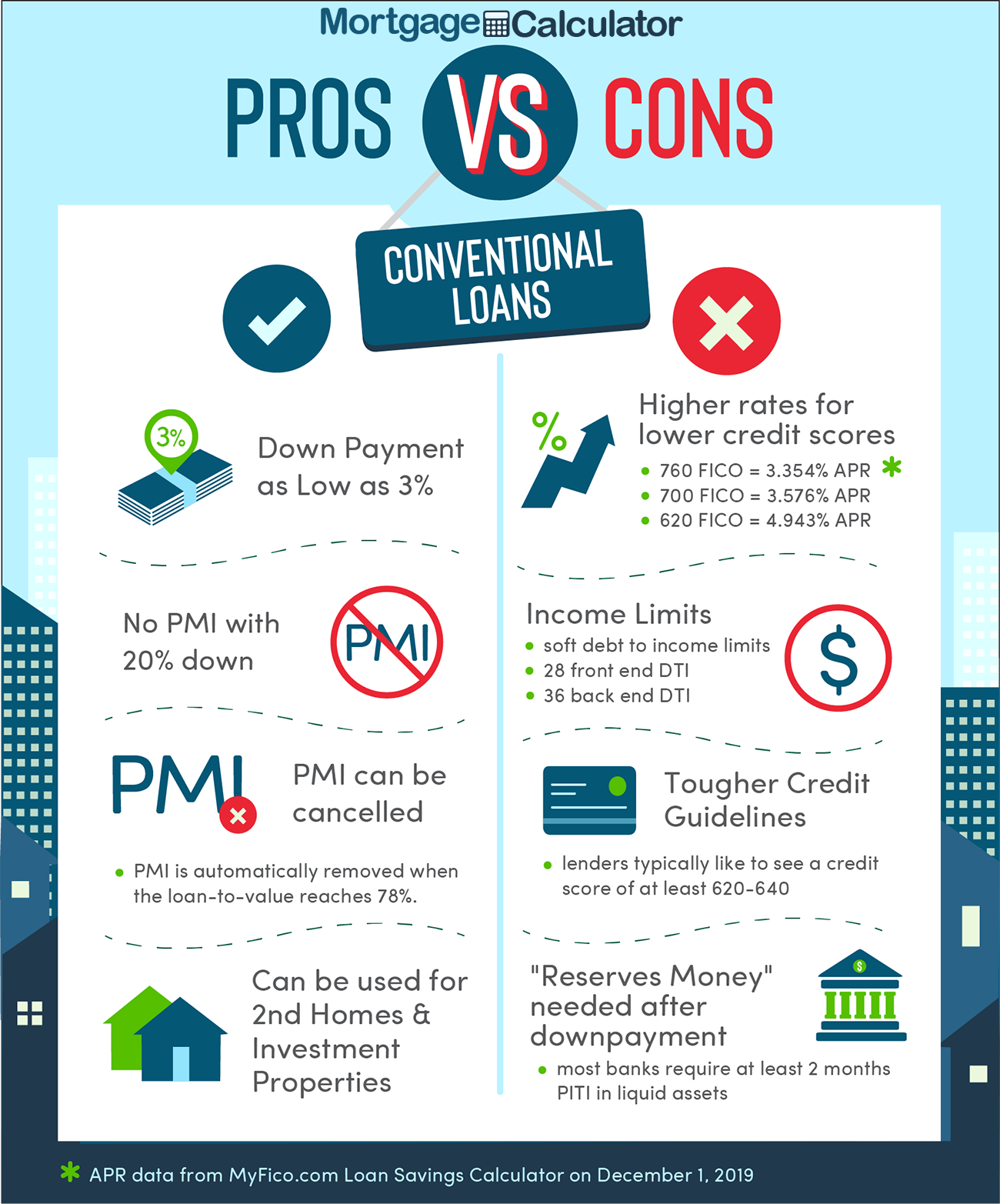

For a Federal Housing Administration (FHA), borrowers normally can make the down payment entirely from donated funds. However, if your credit report falls between 580 and 619, at least 3. 5 percent of the purchase cost need to come from your own cash rather of the donor's funds. If you're pursuing a traditional loan, you can make the down payment completely from the present if you put down a minimum of 20 percent of the purchase rate.

On loans backed by FannieMae or FreddieMac, you can rely entirely on talented funds if you're purchasing a single-family house. You must contribute a minimum of five percent from your own cash if you're obtaining for a two-to-four unit primary home or a 2nd home. Some conventional lenders might require you to consist of some of your own money with the present for the down payment at any time your loan-to-value ratio surpasses 80 percent.